Better Small Business Lending Requires Better Data: Why Implementing Section 1071 Cannot Wait

Women- and minority-owned small businesses play a crucial role in our communities – yet they continue to face lending disparities that prevent them from reaching their full potential.

1. Executive Summary

The persistent challenges and disparities faced by women- and minority-owned small businesses are underscored by a wealth of research on small business lending, as well as the lived experiences of small business owners. Section 1071 of the Dodd-Frank Act (“Section 1071”) was designed to close this gap by requiring financial institutions to compile, maintain, and submit data on credit applications from women- and minority-owned small businesses(1), similar in structure to the long-standing Home Mortgage Disclosure Act (HMDA) for residential lending. In March 2023, the Consumer Financial Protection Bureau (CFPB) finalized rulemaking to implement Section 1071. Since then, compliance deadlines have been repeatedly extended, most recently for another year while legal challenges play out.(2) This continued delay keeps vital small-business lending data out of reach—data that could unlock business potential for Minority and Women-Owned Business Enterprises (MWBEs) and help lenders assess untapped markets, track their performance, and address inequities. Full and timely implementation of Section 1071 is essential to advancing fair lending, strengthening the backbone of an equitable economy, and closing lending disparities for small business owners. It remains a critical tool for transparency, accountability, and inclusive economic growth.

2. Background / Problem

2.1 The Stakes for Small Businesses

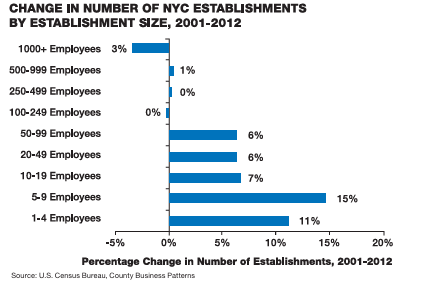

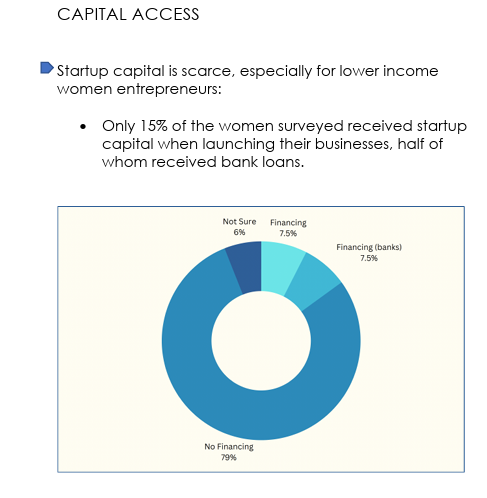

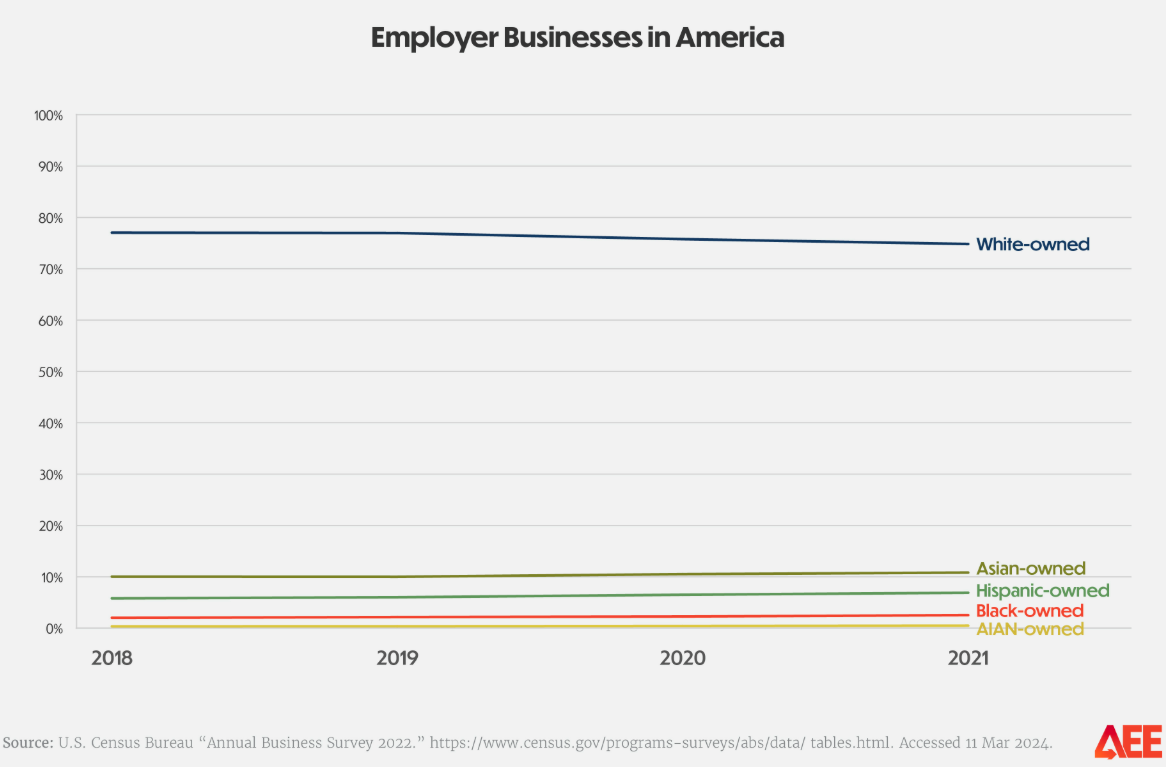

Small businesses are the backbone of New York City’s economy. Of roughly 220,000 businesses, 98 percent employ fewer than 100 people, and 89 percent employ fewer than 20.(3) They anchor neighborhoods, generate jobs, and sustain local economies.  Yet persistent racial and gender disparities remain. Black New Yorkers make up about 22 percent of the city’s population but own only 3.5 percent of NYC businesses.(4) Data from the National Urban League show that only 32 percent of Black-owned businesses are fully approved for financing, compared with 56 percent of white-owned firms; 40 percent of Black-owned businesses are completely denied loans or credit, versus 18 percent of their white-owned counterparts.(5) The National Community Reinvestment Coalition (NCRC) further found that “white testers were given more information from lenders and asked to provide less upfront documentation than Black and Hispanic testers.”(6) Across gender lines, barriers persist. A Women’s Entrepreneur Survey from CDFI lender Accompany Capital in NYC found that only 15 percent of respondents received start-up capital—and just half of that came from bank loans.(7)

Yet persistent racial and gender disparities remain. Black New Yorkers make up about 22 percent of the city’s population but own only 3.5 percent of NYC businesses.(4) Data from the National Urban League show that only 32 percent of Black-owned businesses are fully approved for financing, compared with 56 percent of white-owned firms; 40 percent of Black-owned businesses are completely denied loans or credit, versus 18 percent of their white-owned counterparts.(5) The National Community Reinvestment Coalition (NCRC) further found that “white testers were given more information from lenders and asked to provide less upfront documentation than Black and Hispanic testers.”(6) Across gender lines, barriers persist. A Women’s Entrepreneur Survey from CDFI lender Accompany Capital in NYC found that only 15 percent of respondents received start-up capital—and just half of that came from bank loans.(7)

2.2 A Persistent Data Blind Spot

Most lenders are not required to disclose small-business loan data by race, gender, or ethnicity, and the limited data collected are not public. As a result, banks, regulators, and policymakers lack the information necessary to identify and address disparities. While the Community Reinvestment Act (CRA) tracks lending to small businesses with revenues under $1 million or located in low- and moderate-income census tracts, it does not reveal how credit is distributed across demographic lines. Section 1071 fills this gap—better small business lending requires better data.

2.3 Economic and Policy Consequences of Delay

Years of delays in implementation widen disparities and undermine the financial security of many small businesses. Without comprehensive lending data, we cannot point to disparities in lending and access to credit; additionally, the lack of small business lending data hinders economic growth and the ability to tap into the business potential of small business owners. A study by Citigroup estimates that fair access to lending for Black-owned small businesses alone would have resulted in $650 billion in additional business revenue per year, as well as created an additional 6.1 million jobs per year.(8) The delay also enables alternative loan providers (i.e., non-bank, payday, and fintech lenders), who operate with minimal oversight, higher-cost lending products, and sometimes utilize predatory lending practices, to dominate in the undercapitalized markets and deepen financial inequities.

3. Solution / Recommendations

Implement Section 1071 Without Further Delay

In 2023, the New York State Department of Financial Services (NYSDFS) finalized its own data-collection rule for business lending to minority-owned and women-owned businesses—codified under the NYS CRA(9)—in alignment with the original Section 1071 timeline. This is a positive step at the state level, but federal alignment remains crucial. The CFPB must move forward with full implementation of the 2023 final rule. Timely implementation ensures:

- Better Data → Better Lending:

Lenders can benchmark their performance, identify unmet credit needs, and increase lending to underserved businesses—particularly women- and minority-owned firms.

- Unlocking Economic Growth:

Banks can use disaggregated small business lending information to design more responsive financial products and build stronger relationships with historically underserved communities. More intentional and adaptive lending can expand access for minority- and women-owned businesses, resulting in increased revenue, job creation, and a sustainable local economy.

- Fair Lending & Accountability:

Publicly available data enable regulators, policymakers, and community advocates to assess compliance, ensure fair lending enforcement, and expand community development opportunities.

4. Conclusion

The benefits of having transparent small business data resulting from the timely implementation of Section 1071 are immense and clear. The Section 1071 rule was developed through rigorous analysis and extensive stakeholder engagement through the rulemaking process set forth by the CFPB. The current lack of data in small business lending contributes to persistent gaps in access to credit for small businesses, which in turn decreases economic growth and job creation in New York City. ANHD urges the CFPB to implement Section 1071 immediately. Doing so will provide a full and transparent picture of the small business lending market and access to credit for small businesses, which are the true backbone of America. Better data leads to better lending, and better lending builds economically resilient communities.

(1) “Small Business Lending Rulemaking.” Consumer Financial Protection Bureau, 10 Oct. 2023, www.consumerfinance.gov/1071-rule/ . Accessed 3 Nov. 2025. (2) Earp-Thomas, Maxwell. “CFPB Extends Compliance Deadlines for Section 1071 Small Business Lending Rule.” Consumer Finance and Fintech Blog, 9 Oct. 2025, www.consumerfinanceandfintechblog.com/2025/10/cfpb-extends-compliance-deadlines-for-section-1071-small-business-lending-rule/ . Accessed 3 Nov. 2025. (3) “Small Business First Better Government. Stronger Businesses.” Www.nyc.gov, www.nyc.gov/site/smallbizfirst/download/download-plan.page. Accessed 3 Nov. 2025. (4) “Black Entrepreneurs NYC (BE NYC).” Nyc.gov, 2019, nyc-business.nyc.gov/nycbusiness/business-services/initiatives/black-entrepreneurs-nyc-be-nyc. Accessed 3 Nov. 2025. (5) Monteil, Candece. “Black-Owned Businesses Face Significant Obstacles. Anti-Racial Justice Efforts Are Making Them Worse.” Nul.org, 2024, nul.org/news/black-owned-businesses-face-significant-obstacles-anti-racial-justice-efforts-are-making-them. Accessed 3 Nov. 2025. (6) Less, Amber, et al. “Disinvestment, Discouragement and Inequity in Small Business Lending.» NCRC.” Ncrc.org, 4 Sept. 2019, ncrc.org/disinvestment/ .Accessed 12 Nov. 2025. (7) Gurung, Tshering, et al. “The Accompany Capital NYC Women Entrepreneurs Surveys.” 2023. (8) Peterson, Dana M., and Catherine L. Mann. “Closing the Racial Inequality Gaps.” Citigroup.com, 22 Sept. 2020, www.citigroup.com/global/insights/closing-the-racial-inequality-gaps-20200922. Accessed 3 Nov. 2025. (9) “Superintendent Adrienne A. Harris Adopts Community Reinvestment Act Regulation to Improve Lending to Minority- and Women-Owned Businesses.” Department of Financial Services, 8 Feb. 2023, www.dfs.ny.gov/reports_and_publications/press_releases/pr2023020input 8. Accessed 12 Nov. 2025.